INTRODUCTION

A recent national retirement survey found that only 46% of Canadians feel confident they’ll have enough to retire comfortably, despite most saying retirement is a top financial priority. ¹

Too many investors are approaching retirement without a clear, up-to-date financial plan. Some are relying on outdated strategies while others are skipping planning altogether. This gap puts long-term goals (and peace of mind) at serious risk.

This guide breaks down five of the most common retirement planning mistakes and how to avoid them. Whether you’re still growing your wealth or preparing to live off it, these strategies are designed to help you build a more secure, resilient retirement plan.

This material is for informational purposes only and does not constitute financial advice. For a personalized review of your retirement strategy, contact Bart Chatterson at 306-700-5106 or b.chatterson@iaprivatewealth.ca.

5 COSTLY RETIREMENT PLANNING MISTAKES AND HOW YOU CAN AVOID THEM

In today’s unpredictable economy, standing still can be the biggest risk to your financial future. Inflation is eroding purchasing power, interest rates remain high, and markets continue to swing with global uncertainty.

Many portfolios that looked “good enough” a decade ago have barely kept up especially after taxes and inflation take their toll.

The real danger? Most people either haven’t built a financial plan or are relying on one that’s outdated.

If your strategy hasn’t evolved with the economy, your lifestyle and retirement goals could be slipping out of reach without you even realizing it. Let’s explore 5 common planning mistakes that could derail your future.

Mistake #1: Not Having a Plan

Too many people delay retirement planning until it’s almost too late. They think they’ll figure it out later or avoid it altogether in fear of sacrificing their lifestyle.

But putting it off can quietly erode your future wealth.

We often meet successful entrepreneurs who are great at reinvesting in their business but haven’t mapped out how they’ll exit, fund retirement, or transition wealth tax-efficiently.

Without a plan, you’re likely missing key tax strategies, investment opportunities, and risk protection. You might not know how much you actually need to retire. Or worse, you may be overconfident in your ability to sell your business or rely on passive income that hasn’t been stress-tested.

AVOID THIS TRAP: Get a proactive financial and retirement plan in place.

Make sure it’s managed by experts who understand the complexities of wealth, business ownership, and long-term growth.

Mistake #2: Letting Your Plan Gather Dust

Creating a plan is just the first step. Life changes; so should your strategy.

Factors like tax law changes, market volatility, and shifts in personal circumstances (such as business growth, asset acquisitions, or family changes) necessitate regular plan reviews.

An outdated plan may overlook new tax-saving opportunities, misalign with your current risk tolerance, or fail to account for significant life events.

AVOID THIS TRAP: Review your financial and retirement plans regularly.

Make sure your strategy evolves with your career, family, and financial life. Your plan should work for you, not against you.

Mistake #3: Investing Without a Disciplined System

Study after study shows that the average investor cannot beat the market.

You may have heard that “fear and greed” drive the markets. Investing based on emotions (fear during downturns or greed during rallies) can be costly.

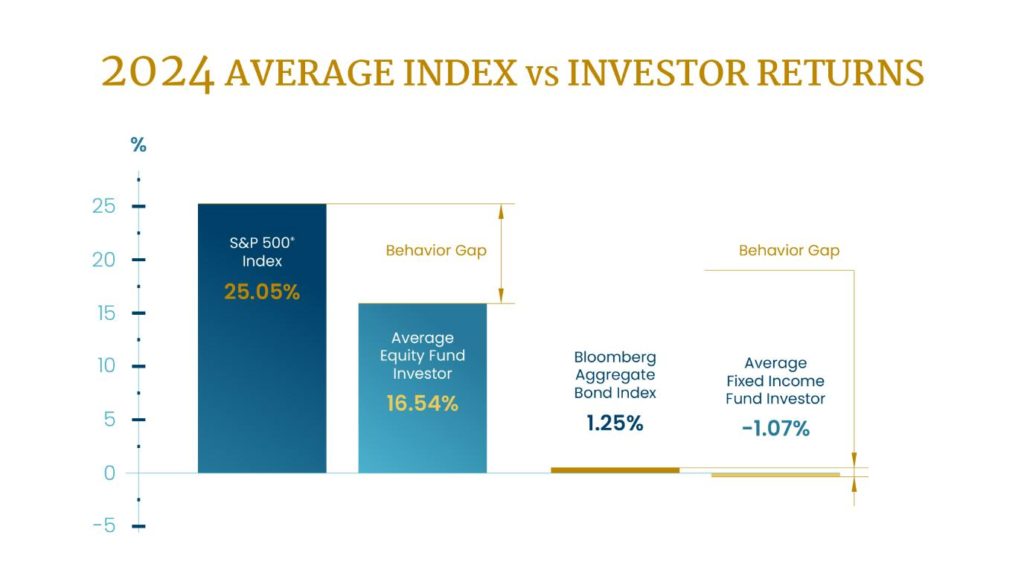

According to DALBAR’s 2025 Quantitative Analysis of Investor Behaviour (QAIB), the average equity investor earned an annualized return of 16.54% in 2024, while the S&P 500 returned 25.05%. The same report states that “This 848-basis point lag is the second-largest investor performance gap of the past decade”.

This gap, often referred to as the “behaviour gap,” highlights the cost of emotional investing.

For business owners and high-net-worth professionals, the stakes are even higher. Without a disciplined investment strategy, the risk of significant underperformance increases, potentially jeopardizing long-term financial goals.

AVOID THIS TRAP: Implement a disciplined, long-term investment strategy aligned with your financial objectives.

Working with a qualified financial advisor can help mitigate emotional decision-making and ensure your investment approach remains consistent and goal oriented.

Mistake #4: Thinking Diversification Alone Keeps You Secure

Many investors believe that simply owning a mix of stocks, bonds, and funds means they’re protected. But diversification (done the traditional way) isn’t enough. If all your assets drop at once in a market downturn, how protected are you really?

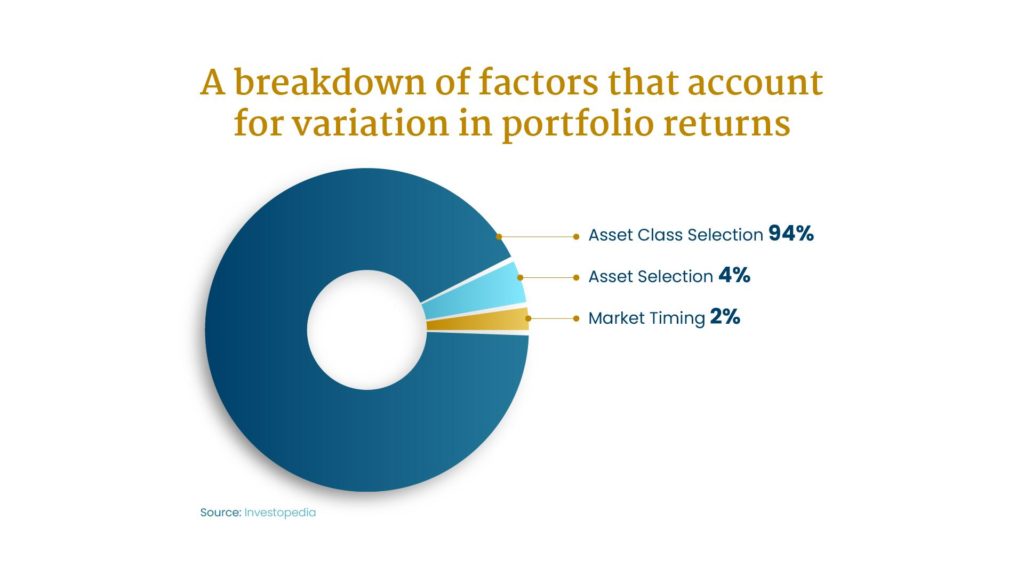

A high correlation exists between the returns investors achieve on their holdings and the underlying asset class performance of those holdings.

- Investopedia, Diversification: It’s All About (Asset) Class

Traditional diversification may give the illusion of protection, but if your assets are moving in the same direction, and that direction is down, you’re still fully exposed.

What makes this worse? Most portfolios overlook four critical risks that can quietly erode your wealth:

- Longevity risk: The longer you live, the more years you’ll need to fund, which increases the risk of your money running out before you do

- Market Risk: Relying too heavily on unpredictable markets can jeopardize your entire portfolio, especially near or in retirement

- Inflation Risk: Even modest inflation steadily erodes your purchasing power, making your money worth less over time

- Point-in-Time Risk: Withdrawing from investments when markets are down locks in losses and can derail your entire plan

Unfortunately, many business owners and professionals haven’t accounted for these risks, which leads to blind spots in their investment strategy, coverage, and long-term financial planning.

AVOID THIS TRAP: Evaluate your portfolio with an expert.

Ensure your portfolio actively avoids declining assets and emphasizes strength, income buffers, and alignment with your retirement timeline. Your retirement savings should be both preserved and positioned for growth.

Mistake #5: Using a "Buy and Hold" Strategy

A set-it-and-forget-it approach may work during wealth accumulation, but it’s risky when you’re approaching or in retirement.

Your financial needs shift in the distribution phase, and with today’s market volatility and frequent economic shocks, a static portfolio won’t cut it.

You need active oversight to stay aligned with evolving market trends, personal circumstances, and economic changes.

AVOID THIS TRAP: Don’t rely on outdated, static investment strategies.

Partner with an advisor who actively manages your portfolio and focuses on market’s strongest assets. This ensures your investments stay aligned with both your retirement income needs and the areas of the market best positioned for growth.

So what makes a plan bulletproof?

Avoiding costly mistakes is only half the equation.

Peace of mind about the future requires a solid strategy that adapts, preserves, and performs. Here are 3 non-negotiables every bulletproof retirement plan should include, regardless of your portfolio size or stage of life.

Why Relative Strength outperforms traditional strategies

To bring these pillars to life—especially investment oversight and risk management—we use a strategy grounded in Relative Strength.

Rather than spreading money across every asset and hoping for recovery, this approach focuses on what’s working right now in the markets. It’s a more active, data-driven method that adapts to change and positions your portfolio to preserve capital while still capturing opportunity.

Here’s why it works:

- It focuses on what’s working now, not just what’s held long-term.

Buy-and-hold assumes all investments will rebound over time, but time isn’t a luxury for investors nearing retirement. Relative Strength Strategy allocate to investments showing strong, consistent performance in current conditions rather than waiting for lagging assets to recover.

- It avoids dead weight.

Diversification spreads your money across multiple sectors or asset classes, but many of those assets may underperform for years. Relative Strength trims the underperformers and concentrates on areas gaining momentum, improving the portfolio’s overall efficiency.

- It adapts to change—economies, interest rates, and global trends.

Buy-and-hold and Diversification assume static portfolios can weather any storm. Relative Strength Strategy is built on regular re-evaluation and rotation into top-performing sectors, asset classes, or geographies as conditions change.

- It supports capital preservation and growth.

In retirement or pre-retirement, avoiding major drawdowns is critical. Relative Strength reduces exposure to declining assets and focuses on those showing strength, helping preserve capital while still capturing upside.

- It’s based on data, not emotion.

Unlike reactive, emotional decision-making, Relative Strength Strategy use objective indicators of performance helping you stay invested with clarity and discipline.

In short:

Buy-and-hold assumes all ships will rise.

Diversification says: Own every ship.

Relative Strength says: Only stay on the ships that are actually sailing.

Relative Strength isn’t just a concept. It’s the cornerstone of how we manage money for clients who can’t afford to rely on outdated strategies or assumptions. But investment selection is just one part of the equation.

To truly retire with confidence, you need a complete system.

One that connects your goals, your income needs, and the right investment strategy into a cohesive plan.

That’s where the RetireSure Process™ comes in.

It’s our proactive, hands-on approach designed for today’s financial realities, so you can build, protect, and enjoy the wealth you’ve worked hard for.

The RetireSure Process™

Helping You Build, Presevre, and Enjoy the Wealth You’ve Worked Hard For

The financial world has changed dramatically over the past decade, but most financial advice hasn’t. That’s why we created the RetireSure Process™. It’s a proactive, hands-on approach designed for today’s environment and built around what matters most to high-achieving professionals and business owners: clarity, control, and confidence.

Our system focuses on three core pillars:

Whether you’re looking to retire confidently, transition your business, or preserve family wealth, the RetireSure Process™ is designed to help you do it with clarity and peace of mind. Let’s unpack what these pillars look like:

Strategy #1: A Custom Financial Plan

Your financial journey starts with one thing: you. Your goals, values, lifestyle, and legacy shape how your plan should be built.

In our Big Picture Meeting, we ask the right questions to uncover your concerns, priorities, and vision for the future.

This helps us understand both the emotional and financial aspects of your situation, because a truly effective plan needs to consider more than just numbers.

From there, we act as your personal CFO—coordinating with your legal, tax, and estate professionals so you can focus on what matters while we take care of the details.

We proactively manage risk, optimize your income and insurance coverage, and help preserve your wealth for generations.

If your current advisors aren’t asking these questions, or if your plan hasn’t been updated to reflect your life today, it’s time for a smarter, more aligned approach.

Strategy #2 – A Custom Investment Management

Strategy Based on Your Plan

Smart investing means aligning your portfolio with your goals, tax situation, cash flow needs, and risk comfort. Too many people skip this step, or base decisions on emotion.

Our process removes the guesswork. We follow a data-driven approach rooted in market strength, focusing on what’s performing well and steering clear of what’s not.

Instead of betting on a rebound, we stay with strong performers until the numbers say otherwise. Whether you’re building wealth or living off it, we design portfolios that work for your life stage and balances growth, preservation, and income.

And we never “set it and forget it.” Your investments evolve with the market, your life, and your goals.

Strategy #3 — Ongoing Investment and Financial Plan Management

Your plan isn’t one-size-fits-all. It’s living, breathing, and unique—like a fingerprint. Once your strategy is in place, we proactively monitor it and adapt as needed to keep you on track.

From shifting markets to life changes, we stay ahead of what’s next, so you don’t have to. With regular check-ins, updates, and clear communication, you stay informed and confident in every step forward.

So what you can do right now?

Book a No-Obligation Review of Your Retirement Plan and Investments

With inflation, market volatility, and rising interest rates continuing to challenge investors, now is the time to make sure your financial plan is still working for you.

Book your Big Picture Retirement Review with Bart Chatterson—a no-pressure, personalized conversation to assess where you are, where you want to be, and whether your current plan gets you there.

Here’s what you’ll gain from this one-on-one session:

- Clarity on Your Financial Position

We’ll walk through a short questionnaire to identify your key goals, income needs, and concerns and see if you’re on track to fund the retirement you want. - A Portfolio Check-Up

We’ll review your current investments, highlight risks and opportunities, and benchmark performance, so you know exactly how your money is working for you (in plain English, not industry jargon). - A Practical Action Plan

If we find gaps, you’ll leave with prioritized recommendations and next steps to help grow and protect your wealth through retirement and beyond.

During the review, we’ll address key questions like:

- Are your investments positioned for both growth and downside protection?

- Could your estate plan, insurance, or withdrawal strategy use an update?

- Are you set up to retire confidently and stay retired, without running out of money?

- What changes can help reduce risk while still supporting your lifestyle goals?

If you’re preparing for retirement, worried about your current investment strategy, or simply want an objective second opinion, this review is for you.

Take the first step.

Schedule your free Big Picture Retirement Review by calling 306-700-5106, or emailing b.chatterson@iaprivatewealth.ca.

There’s no obligation—just a smarter way to make sure your money is working as hard as you are.

This information has been prepared by Bart Chatterson, who is a Portfolio Manager for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the Bart Chatterson, B.Comm, CIM ® Portfolio Manager, iA Private Wealth securities mentioned. The information contained herein may not apply to all types of investors. The Portfolio Manager can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.

About Bart Chatterson, CIM®, PFP, B.Comm